How to Avoid Foreign Transaction Fees in Europe: Save 3-5% on Every Purchase

Stop losing 3-5% on cross-border shopping. Best fee-free cards for Europe (Monzo, Starling, Chase), currency tips, and payment strategies that save £200-400/year.

TL;DR: What The Numbers Tell You

- Cross-border purchases add 3-5% in hidden costs through foreign transaction fees—that’s £30-£50 lost on every £1,000 spent internationally.

- Fee-free cards exist from providers like Monzo, Starling, and Chase, eliminating this cost entirely with proper selection.

- The real expense includes both card fees and unfavourable exchange rates; understanding both components cuts total costs by up to 7%.

- Strategic payment selection saves roughly £200-£400 annually for frequent cross-border shoppers.

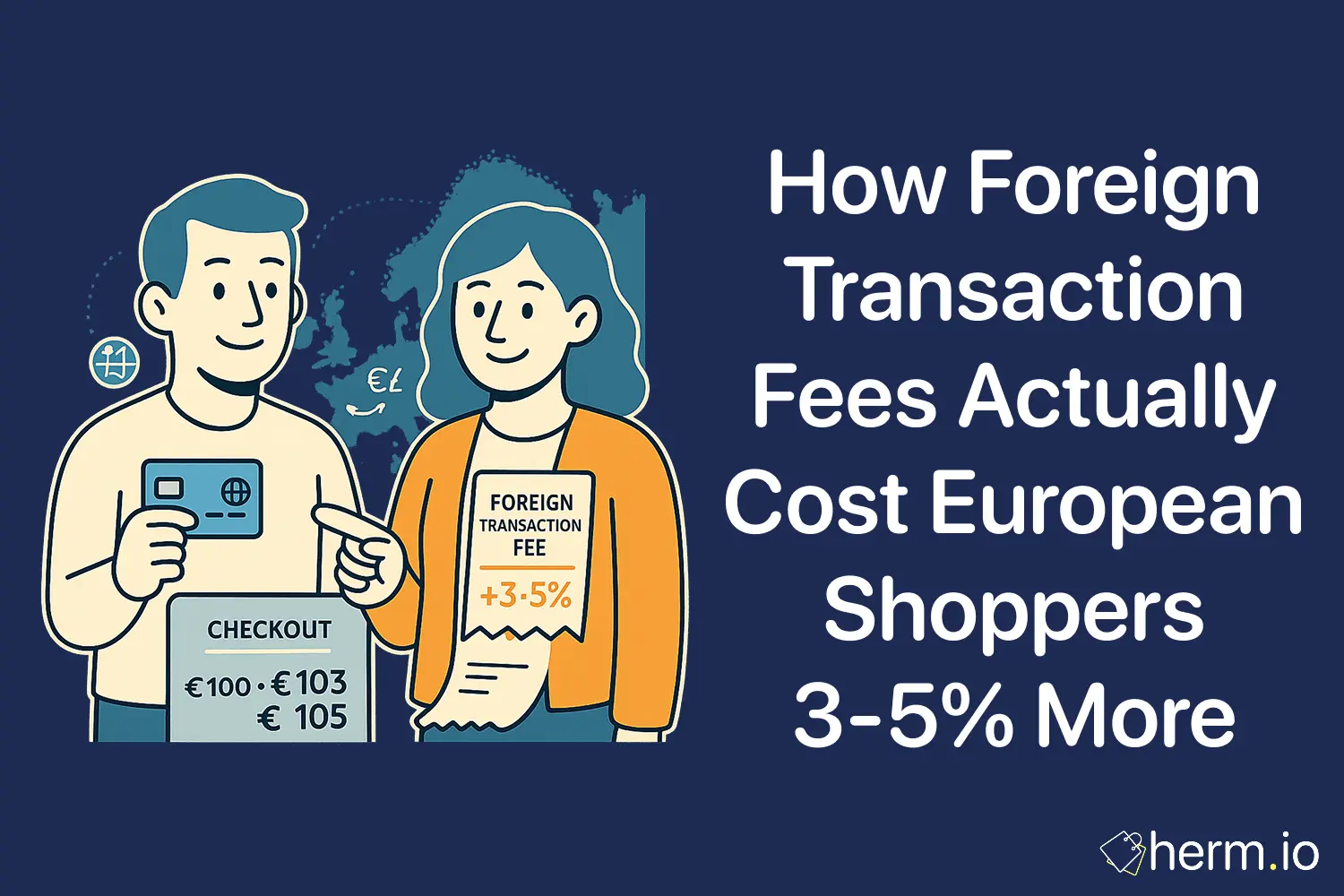

The numbers reveal something most shoppers miss: a £100 purchase from a non-UK retailer actually costs £103-£105 when fees compound. That 3-5% differential represents pure inefficiency in payment selection.

European e-commerce has built structural complexity into cross-border transactions. Each purchase involves two distinct cost layers—the explicit foreign transaction fee and the implicit currency conversion markup. Most shoppers see only the final charge; understanding the component breakdown changes purchasing behaviour significantly.

Quick Wins: Implement These Today

- Switch to fee-free cards for all cross-border purchases (setup time: 15 minutes, potential annual savings: £200-£400)

- Compare exchange rates between payment methods before checkout

- Enable multi-currency accounts for frequent international shopping

- Track actual costs versus displayed prices to quantify hidden fees

- Set payment defaults to fee-free options in browser settings

Understanding The Two-Part Cost Structure

Foreign transaction fees don’t work as single charges. The system breaks into two components, each extracting value separately.

The explicit fee appears as a percentage—typically 2.75-2.99% for most UK cards. Purchase something for €100, and your statement shows an additional £2.50-£3 charge. That’s the visible cost.

The implicit markup hides in exchange rates. Card networks apply their own conversion rates, usually 1-3% worse than interbank rates. A €100 item converts at a padded rate, making you pay £88 instead of £86. The £2 difference never appears as a separate line item; it’s absorbed into the total.

Combined, these mechanisms create a 3-7% premium on cross-border purchases. On £5,000 in annual international shopping, that’s £150-£350 in avoidable costs.

Cards Without Foreign Transaction Fees

Several providers have eliminated foreign transaction fees entirely, restructuring their economics around other revenue streams.

Monzo and Starling Bank charge 0% on cross-border transactions up to £200 daily, using near-interbank exchange rates. The rate markup sits around 0.3-0.5%—significantly better than traditional banks. For purchases above £200 daily, a small percentage fee applies, but the threshold covers most shopping scenarios.

Chase’s debit and credit cards offer unlimited fee-free foreign transactions with competitive exchange rates. The card processes payments at rates within 0.5% of interbank, making it optimal for larger international purchases.

Revolut provides fee-free transactions up to £1,000 monthly on standard accounts, with weekend exchange rate markups the main consideration. The tiered structure works well for moderate cross-border shopping volumes.

These options share a common mathematical advantage: they eliminate the explicit fee entirely and minimize the implicit markup. The combined benefit approaches 3-5% per transaction.

The Currency Selection Framework

Payment processors present a choice at checkout: pay in your home currency or the merchant’s currency. This decision carries significant cost implications.

Dynamic currency conversion (DCC) lets you pay in pounds when shopping from European retailers. It seems convenient—you see the exact pound amount before confirming. The conversion rates, however, typically add 3-6% to the true cost. That €100 item might show as £92 instead of the £86 it should actually cost.

The mathematically optimal choice selects the merchant’s currency. Your card provider then handles conversion, usually at better rates than the merchant’s processor offers. Even with a 2.75% foreign transaction fee, paying in euros often costs less than accepting DCC in pounds.

The calculation framework: compare the DCC rate against your card’s fee plus its exchange rate markup. If your fee-free card uses rates within 0.5% of interbank, paying in merchant currency saves 3-5.5% versus accepting DCC.

Calculating True Cross-Border Costs

Transparency requires breaking down the actual mathematics of international purchases.

Start with the interbank rate—the baseline exchange rate banks use amongst themselves. On a given day, this might be £1 = €1.16. That’s your reference point.

Add your card’s explicit foreign transaction fee. For a standard UK credit card at 2.99%, a €100 purchase becomes £86.21 × 1.0299 = £88.79.

Factor in the exchange rate markup. If your card converts at £1 = €1.14 instead of €1.16, you’re paying an additional 1.7%. The €100 item now costs £87.72 before the fee, or £90.34 after.

Compare this against a fee-free card using near-interbank rates. The same €100 converts at approximately £86.50—a £3.84 difference per €100 spent. Scale that across annual spending patterns to quantify total impact.

The differential compounds with purchase frequency. Monthly €500 in cross-border shopping represents £230 in annual avoidable costs when using traditional cards versus fee-free alternatives.

Alternative Payment Methods Beyond Cards

Several non-card payment structures minimize cross-border transaction costs through different mechanisms.

Wise (formerly TransferWise) offers a multi-currency account with a debit card. It holds balances in multiple currencies and converts between them at rates within 0.35-0.45% of interbank. For planned international purchases, loading the relevant currency in advance locks in rates and eliminates conversion timing risk.

PayPal’s buyer fees vary by transaction, but connecting a fee-free card as the payment source preserves the cost advantage. The additional layer adds minimal friction whilst maintaining optimal rates.

Bank transfers work for larger purchases where retailers accept them. SEPA transfers between European accounts cost £0-£5 typically, making them efficient for purchases above £500 where percentage-based fees become expensive.

Each method suits different purchasing patterns. Card payments offer convenience for varied, frequent purchases. Multi-currency accounts optimize for regular shopping from specific regions. Transfers work best for planned, larger transactions where setup time justifies the savings.

Implementation Strategy For Cross-Border Shopping

Converting this analysis into action requires systematic payment restructuring.

Open accounts with 2-3 fee-free card providers. Monzo or Starling serve as primary cards for purchases under £200 daily. Chase handles larger transactions. This redundancy ensures payment flexibility whilst maintaining cost optimization.

Set these cards as default payment methods in browser settings and with frequent retailers. Most browsers and e-commerce platforms remember payment preferences, reducing friction in future transactions.

Enable spending notifications and monthly summaries to track actual foreign transaction costs. Both Monzo and Starling provide detailed breakdowns showing exchange rates applied and total fees. This data validates whether optimization efforts translate into measured savings.

For retailers you purchase from regularly, consider whether they offer local subsidiaries. Amazon, for instance, has separate UK and European operations. Purchasing from Amazon.co.uk instead of Amazon.de eliminates foreign transaction considerations entirely, though product availability and pricing may vary.

Calculate quarterly savings by comparing current foreign transaction costs against historical patterns. The baseline establishes ROI for this payment optimization effort.

FAQs About Cross-Border Payment Costs

How do I know if my current card charges foreign transaction fees?

Check your card’s terms or review recent statements from international purchases. Foreign transaction fees appear as separate line items labelled “non-sterling transaction fee” or similar. If you don’t see them but notice purchases cost slightly more than expected, your card likely applies fees within the exchange rate itself. Contact your card provider for explicit fee structures.

Are there situations where fee-charging cards make sense for international purchases?

Premium cards offering significant rewards (2%+ cashback or valuable points) can offset foreign transaction fees through rewards. The calculation compares fee percentages against reward value—if you earn 2.5% back on a card with a 2.75% fee, the net cost becomes 0.25%. Factor in whether you’d actually use the rewards earned. Cash savings from fee-free cards require no redemption effort.

Do exchange rates fluctuate enough to make timing my purchases worthwhile?

Exchange rate volatility typically ranges 1-2% weekly for major currency pairs like GBP/EUR. For large planned purchases (£500+), monitoring rates for 1-2 weeks can capture favourable movements. For routine shopping, the effort rarely justifies potential savings; the consistent benefit from fee-free cards outweighs tactical timing in most scenarios.

How do business purchases differ from personal cross-border shopping?

Business cards often include higher foreign transaction fees (2.99-3.5%) but may offer expense tracking benefits that justify the cost. Some business accounts provide multi-currency functionality or better rates for frequent international transactions. The optimization framework remains similar: calculate total annual foreign transaction costs, compare against alternative payment methods, and select based on net benefit including administrative efficiency.

The mathematics of cross-border shopping creates clear pathways for cost reduction. Fee-free cards and strategic payment selection eliminate 3-5% in transaction costs—a structural advantage that compounds with every international purchase. The implementation requires minimal effort: open the right accounts, update payment defaults, and let the system work. The numbers handle the rest.

What is the best card for no foreign transaction fees in Europe?

In the UK, Monzo, Starling Bank, and Chase offer zero foreign transaction fees on purchases and ATM withdrawals in Europe. For daily spending under £200, Monzo or Starling work well. For larger purchases, Chase provides similar benefits with additional cashback. Revolut offers fee-free spending up to a monthly limit, after which a small markup applies. Always check current terms as these can change.

Should I pay in local currency or my home currency when shopping abroad?

Always choose the local currency (e.g., EUR in France, SEK in Sweden). When a terminal asks “Pay in GBP?” or “Pay in your home currency?”, decline — this is Dynamic Currency Conversion (DCC), and the markup is typically 3-5% worse than your bank’s own exchange rate. This applies to both in-store card payments and online purchases from foreign retailers.

Written by

Camille Durand

Contributor

I'm a marketing analytics expert and data scientist with a background in civil engineering. I specialize in helping businesses make data-driven decisions through statistical insights.

More from CamilleRelated Articles

Your Complete Guide to Finding Clearpay Shops Online in 2026

Find Clearpay shops online in 2026: official directory, Clearpay Card for in-store & category shortcuts for fashion, beauty & tech.

How to Set Up a TikTok Shop: Your Complete UK Launch Guide for 2026

Learn how to set up a TikTok Shop in the UK with this complete 2026 guide covering registration, fees, Shopify integration, and your first-week launch strategy.

Price Comparison Tools That Work in Europe

Discover which price comparison tools work best in Europe and learn a practical framework for finding genuine deals without hidden costs.